Cramer Wants to Spoon You

Cramer Wants to Spoon You

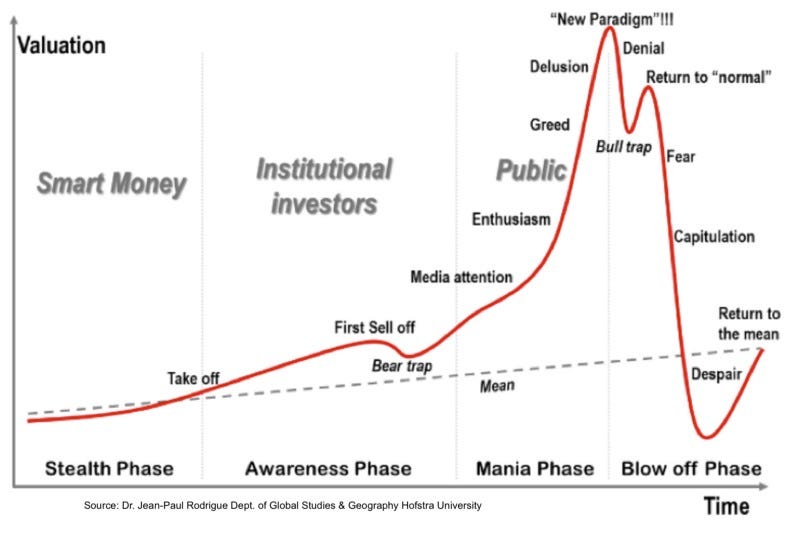

Bend your Understanding of Cycles, Time Horizons, and Liquidity

“Do not try and bend the spoon—that's impossible. Instead, only try to realize the truth.” - Young Monk in The Matrix

Talking Heads (Road to Nowhere)

No one can tell you, with 100% certainty, what the future holds – not even the talking heads on mainstream financial news media. Fund managers step into the spotlight, talking their book – having already placed their bets, they convince you to buy into their selling.

Consider the Bloomberg headline on October 13th, 2021 - Goldman Is ‘Doubling Down’ on Technology Investing, Dees Says:

“We’re doubling down on everything in technology right now,” Dees said. “It’s such an exciting time.”

A sharp contrast to the CNBC headline three months later on January 11th, 2022 - Goldman’s David Kostin says a tech disconnect is the ‘single greatest mispricing’ in U.S. stocks:

“You’ve had a huge derating of the fast expected revenue growth companies that have low margins, and the argument is probably that there is more to go in that readjustment.”

Buying into the Goldman Sachs Future Tech Leaders Equity ETF (GTEK) at the October 2021 headline and selling at the January 2022 headline, would have lost about 4%.

The hedge fund community dumped tech stocks in the four sessions between Dec. 30 and Tuesday as interest rates spiked. The four-session tech unloading marked the biggest sale in dollar terms in more than 10 years, reaching a record since Goldman Sachs’ prime brokerage started tracking the data.

Was Goldman Sachs, employing some of the brightest in finance, caught swimming naked? And not considering low margins in October? The truth is, the rotation out of tech stocks has been on the investment radar since early 2021. Goldman was simply trying to squeeze the last bit of juice out of their long tech narrative as they rotate from low margin tech into the next play.

This is why mainstream financial media is best used as narrative and sentiment indicators – not trading advice.

Trading headlines is the reason retail investors are so commonly referred to as the dumb money – or the greater fool. Retail investors trying to play according to institutional rules (short time horizons) are typically the last ones to the party (late in the cycle). Hedge funds sell to the greater fool – the dumb money, who are left filling the role of both liquidity provider and bag holder. This is why there is no edge for retail investors in trading headlines.

And there is certainly no edge in trading Jim Cramer’s picks (still waiting for someone to develop the inverse Cramer ETF). He does not want you to realize the truth. He does not want you to bend the spoon. However, Cramer would love to spoon you and for $499/yr he will will wrap his loving arms around you, rock you to sleep, and lightly tickle your ear with whispers of horribly wrong predictions.

Do some investors make money chasing the news? Sure, some do, especially in frothy markets. They are often featured on financial news to give you hope. Don’t you see? You can do it too!

The truth, they are speculating on a tightrope – and when the winds of institutional selling begin to blow, well, it’s a long way down.

Cycles

Every bet placed in the market is one of speculation. At its core, each bet should be a guess to where future dollars will flow. In order to make money, you need a whole lotta someones to buy in after you at a higher price. Thus, skating to where the puck is going requires understanding where we are now in the economic cycle (How the Economic Machine Works in 30 minutes by Ray Dalio).

It also requires contrarian and second-level thinking. Both can help you identify an investment thesis within larger cycles, themes, and rotations. The ability to see beyond current sentiment and recognize the divergence between stock price and economic fundamentals is where asymmetric opportunities hide. This mispricing is where inefficiencies rear their head, poking fun at the academically touted efficient market hypothesis.

Diligent research leading to high conviction in these inefficiencies provide an opportunity to be the smart money - to flip the script by front running the flows from both institutional investors and headline chasing retail investors.

These opportunities allow for asymmetric bets - risk $1 for $10. Asymmetric bets are in contrast to day trading, where most retail traders are more commonly risking $10 for $1 (forcing tight risk parameters that fail to allow their position to breathe with market volatility).

Sounds easy enough, right? Buy low, sell high! Ask yourself though, are you really comfortable buying into a thesis that’s hated, spit on, starved of capital, and left for dead on the side of the road? Are you ok with being one of the few people on the other side of the boat? The one ignored as your co-workers brag about the gains from their favorite growth or meme stock?

Warren Buffett famously said:

This is the one thing I can never understand. To refer to a personal taste of mine, I’m going to buy hamburgers the rest of my life. When hamburgers go down in price, we sing “Hallelujah Chorus” in the Buffett household. When hamburgers go up, we weep. For most people, it’s the same way with everything in life they will be buying – except stocks. When stocks go down and you can get more for your money, people don’t like them anymore.

Time Horizon

You may be thinking – how can I recognize these opportunities before institutional investors? You know, the crème de la crème. The truth is, you probably can’t.

However, you can act and dollar-cost average into a position ahead of them by refusing to play by their rules - by implementing a longer 3-5 year time horizon.

Institutional money managers are handcuffed to their client’s desires – which are often motivated by greed and/or impatience. High dollar accredited investors and pension fund managers frequently ask their money managers - what have you done for me this year? Heck, what have you done for me this quarter???

Hedge funds make money by charging fees - the holy grail of two and twenty. Failure, at the very least, to beat the S&P 500 benchmark will result in an outflow of money from the fund, resulting in a drastic blow to their fees and reputation. In other words, they are forced to trade (play their hand) in a short-term time horizon (typically 1 year or less) - or risk losing clients.

In 2016, Dr. Wesley Gray of alpha architect designed a “God” study and applied it to professional active fund managers. His question and results?

If God is omnipotent, could He create a long-term active investment strategy fund that was so good that He could never get fired?

The answer is striking: God would get fired.

Perfect foresight has great returns, but gut-wrenching drawdowns. In other words, an active investor who was clairvoyant (i.e. “God”), and knew ahead of time exactly which stocks were going to be long-term winners and long-term losers, would likely get fired many times over if they were managing other people’s money.

As many investment pros painfully recognize, managing money is often not about absolute performance, but relative short-term performance.

Read Dr. Gray’s full study here.

Liquidity

There are some smaller institutional funds playing the larger 3–5-year time horizon. They stress to investors the importance of patience and holding through volatility, the potential for short-term drag on their portfolio, and the possibility of significant drawdowns. However, they too are handcuffed by liquidity.

In short, liquidity begs the question – if needed, how quickly can I pull money out of this position?

Let’s say company ABC trades with an average volume of 1 million shares per day. Additionally, let’s say, in order to meet target returns, XYZ Fund needs a position of 800,000 shares in company ABC. Attempting to own 80% of the daily volume of traded shares prevents them from building or exiting their position quickly without significantly moving the underlying price of the security against them. And that’s a risk they cannot take.

In other words, the door is too small and needs to expand before they can begin walking through.

We can begin see how liquidity is relative. Constraints to larger funds can be advantageous to the small retail investor. Stock ABC is considered illiquid to XYZ Fund. However, the small retail investor can walk through a small door and build a position of 10,000 shares, owning only 1% of ABC’s daily volume - taking on significantly less liquidity risk.

If the thesis for stock ABC proves true, the daily volume (along with stock price and market cap) will slowly increase over time. Allowing, small institutional funds to participate first - and soon followed by larger institutional funds.

Additionally, the small retail investor can dollar-cost average into the growing volume without losing the option for liquidity.

Eventually, the talking heads will show up on CNBC, pronouncing the thesis as the trade of year. Your co-workers and Uber drivers will happily educate you on why this particular stock or sector is headed for the moon.

At this point, EdgyFin has already sold and is working on the next (hated) thesis – and hopefully you are too.

Consider this simple historical example…

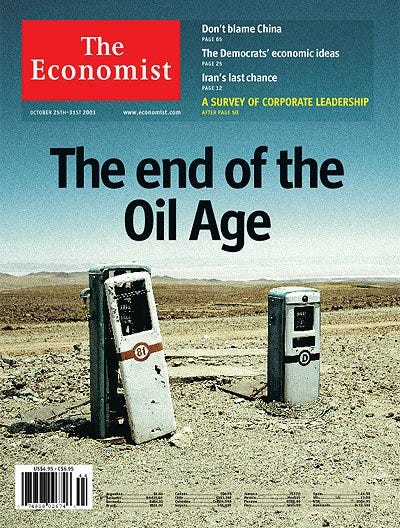

In October of 2003, The Economist proudly announced “The End of the Oil Age” – at which time the West Texas Intermediate (WTI) crude oil price was hitting $29/barrel. Oil, at the time, was hated and starved of capital investments. No capital = lower exploration and production leading to supply constraints.

Over the next five years, the WTI price proceeds to rip to a high of $140/barrel. Why? Despite the 2003 oil price and The Economist’s prediction, the demand from developing countries, technology growth, and the 72+ million U.S. millennials coming of age continued on its path. And the supply just wasn’t there to meet the demand.

The price of oil and the economic fundamentals were disconnected.

There you have it – a broad overview of my EDGE.

In the next post – I’ll begin outlining the process for drilling down into big themes - to find gems that have real value. I’ll also explore the concepts of conviction, position sizing, and managing risk.

I want to offer transparent disclosure:

My active account is where I hunt for outperformance and asymmetric returns with the goal of inching closer to financial freedom. My active account is separate from my retirement portfolio (pension, 401(k), and Roth IRA). I don’t trade on margin and I don’t leverage my real assets for trading capital. In other words, YOLO is a NO, NO!

Before actively managing one dime, I spent years reading everything I could get my hands on, listening to countless interviews with some of the brightest minds in finance, and set up a practice (paper trading) account. Filling in the gaps of my self-education, I enrolled in graduate school and I am currently completing an MBA in finance. And still, most days, I feel as though I’ve just barely scratched the surface of understanding these complex markets – and I’m ok with that.

It’s important to stay humble and to discern luck from a well-executed strategy. Failure to do so and the market will bring you to your knees begging for forgiveness.

And as always, swim with caution!

@EdgyFin on Twitter

Today’s recommended readings:

The Most Important Thing Illuminated: Uncommon Sense for the Thoughtful Investor by Howard Marks

Today’s recommended podcast:

Episode 338. The Tim Ferriss Show: Howard Marks – How to Invest with Clear Thinking

Disclaimer: EdgyFin is for educational purposes only and should not be considered investment advice. Please do your own due diligence and consult with a professional before you risk it for the biscuit!